本月,比特幣經歷了一輪牛市,讓人回想起2017年的情景,當時的數字貨幣往往會達到新的峰值,之后似乎還會進一步走高。

每個人都記得高峰,卻很容易忘記低谷。比特幣的價格通常會隨著價格的上漲而下降。波動性是比特幣從利基市場的無名小卒崛起為全球寵兒的因素之一。在比特幣的最新一輪表現中,波動再次出現。

自去年夏天以來首次突破8000美元大關后,比特幣大幅下跌比特幣,跌至近7000美元,再次証明波動性在比特幣的瘋狂成熟過程中發揮了重要作用。

當然,波動性不僅僅是比特幣的問題。許多最受歡迎的數字代幣都受到價格快速上漲和大幅貶值的困擾,這使得它們實際上無法作為貨幣使用,淪為投機資產。

對於許多業內人士來說,解決這種波動性的辦法一直是使用穩定幣。使用與其他加密貨幣相同的技術,這些代幣的價值與有形資產 (如法幣、金屬或其他資源) 挂鉤。它們是對沖加密貨幣生態系統波動性的一種流行方式,而且它們的功能可能會顯著超過那些更不穩定的同類產品。

實際上,它們保留了數字貨幣的安全性、功能性和可用性,同時提供了更成熟資產的價格可靠性。

這是一個很好的解決方案,但這個行業肯定不是完美的。不過,因為這可以解決加密貨幣最緊迫的問題,穩定幣就可以成為加密貨幣運動不可或缺的二把手。

首先,我們要理解問題所在。以下闡述了穩定幣的兩個缺點,以及穩定幣對加密貨幣的意義。

監管立場

大多數人認為,監管的不確定性對加密貨幣在各個層面的應用都具有重要意義,但對於穩定幣來說,這是一個特別具有先見之明的問題。

因為穩定幣擁有某種程度上的資產挂鉤,它們承載著承諾,因而可以將這類代幣歸類為証券。正如美國証券交易委員會 (SEC) 數字資產高級顧問瓦萊麗•什切潘尼克 (Valerie Szczepanik) 在西南証券交易所 (SXSW) 所說的那樣,“正是這種由一個中央控制價格隨時間波動的項目,可能正在進入証券領域。

今年3月,SEC主席杰伊•克萊頓 (Jay Clayton) 宣布,SEC認為以太坊和其他類似代幣不是証券。在一封較早前的公開信中,克萊頓指出,在加密貨幣的范疇裡,証券的定義變化不定。

雖然這為以太坊等平台指明了道路,但穩定幣仍在等待監管部門的監管,監管可能決定穩定幣行業未來的發展。

更具體地說,有關資產核查、公司溝通和其他標准的規定,可以為穩定幣平台將自己定位於主流、受監管的金融和商業生態系統的整合鋪平道路。

糟糕的公關

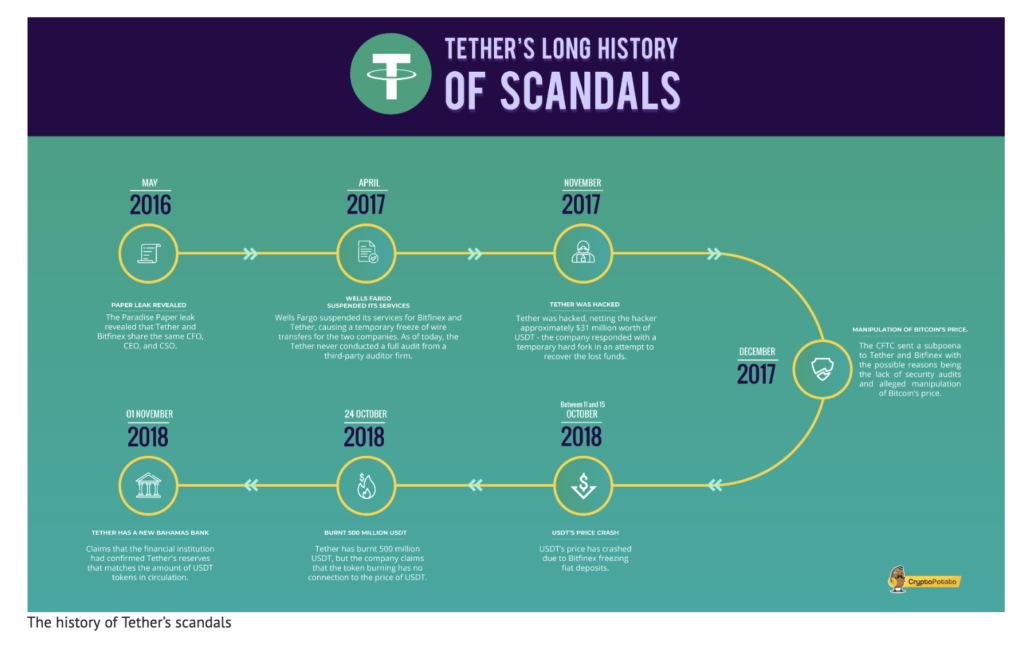

不幸的是,最著名的穩定幣,Tether,正在不斷陷入爭議之中。

Tether一度聲稱其銀行賬戶中每發行一個代幣就持有1美元。評論家們常常不相信這種說法,今年Tether更新其網站時,他們的懷疑得到了証實。

網站解釋說:“每一項貸款都是由我們的准備金100%支持的,包括傳統貨幣和現金等價物,有時還可能包括其他資產和應收賬款,這些資產和應收賬款來自Tether向第三方發放的貸款,其中可能包括關聯實體。”

最近,Tether和隸屬於同一母公司的加密貨幣交易所Bitfinex合謀掩蓋了交易所造成的8.5億美元損失。

穩定幣的目的是贏得用戶的信任,而他們最大的代言人卻一再未能向全球用戶傳達這一點。

However, as Forbes concluded after Tether’s most recent debacle, “despite these legitimate concerns about Tether’s operations, the value proposition of its business model is strong.”

換句話說,Tether的平台可能為其他平台打開了一扇門,讓它們呈現出更可用、更可靠的穩定幣形式。這種產品當然有需求。

未來會怎樣?

顯然,不僅對數字貨幣的總體需求在增長,對穩定幣的需求也在增長。Tether擁有近30億美元的市值,其穩定的價值使其成為加密貨幣交易的熱門中間人。

雖然它在過去的不良行為中相對不受影響,但它能否保持作為最突出的穩定幣的地位,目前還沒有定論。相反,這些代幣有機會通過創建高度可用、完全可審計和廣泛可用的穩定幣,來促進金融和商業的未來發展。

在一個已經將大部分交易放在網上的數字時代,使用一種高度靈活、完全可靠的數字貨幣似乎是最合適的時機。

穩定幣也有自己的問題,但已經有現成的解決方案,如果得到採納,將對加密貨幣行業的發展大有裨益。

0")